The Mortgage Minute |

|

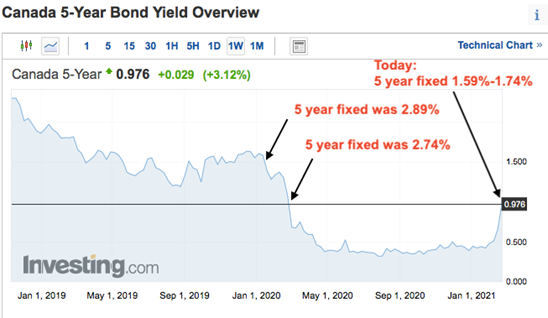

You may be seeing headlines talking about “rate hikes”, or “massive rate jumps”, and in my opinion those are over-reactions. However, several lenders have already increased their 5 year fixed rates this week (one went from 1.64% to 1.74% on Tuesday, and then last night to 1.94%). Other lenders went from 1.64% to 1.69% and stayed there. I still have several lenders that are at 1.59%-1.64% for an insured 5 year fixed term, however the writing is on the wall that the rates below 1.75% will likely rise a little bit. You may recall from some of my previous emails that I have said that 5 year fixed mortgages rates are tied closely to the 5 year Canada bond yields, and so prior to the pandemic if you asked me what would happen to rates, I would look at the bond yield activity and give you my prediction. Once Covid-19 hit, the relationship between the bond yields and fixed rates got a bit out of whack, but it is still good to look at when understanding rates, and get a rough idea of where rates are going. The rough rule of thumb is that the “best rates” are typically 1.5% higher then the bond yields. This is because the lenders often buy the bonds for 5 years, and then use the bonds to fund 5 year mortgage terms. The lenders buy the bonds, and then typically tack on 1.5% (for their profit margins and risk), and that is roughly the interest rate they give the client. So if you look back at January 1, 2020, the bond yields were at roughly 1.5, and 5 year fixed rates were in the 2.89%-2.99% arena which would mathematically make sense based on their profit margins (1.5% plus 1.5% = 3%).  If you look at the bond yields during 2020 (below) you will see that they hovered between 0.4% and 0.5% for most of the year. So add on the spread that the lender needs to bake in for risk and profits, then we would be roughly at 1.9% - 2% for 5 year fixed rates. Since summer that is exactly where rates have been, in that 1.74 – 2.14% range, and several weeks ago they dropped further to 1.59%-1.64%.

Now if you look at the bond activity in the last month, you will see that the cost to purchase bonds has doubled (if you want to know more about why this is happening, you can always call or email me, but I wont’ bore you with the details now), which would indicate the lenders need to increase their rates to keep their shareholders happy. With all this being said, I wouldn’t freak out. It seems to be a normal regression to the mean as there has been more and more positive news in North America lately (e.g., vaccines, political stability, and unemployment) I think I’ve already shared enough, so I won’t go into details, but we don’t expect to see changes to variable rates (those are tied more closely to the BoC’s overnight lending rate, and the BoC has said they don’t intend on making significant changes until 2023). Don’t hesitate to reach out with any questions,

0 Comments

Leave a Reply. |

AuthorPaul holds a Master's degree in Business Administration, loves to golf, watch hockey, and drink black coffee. Archives

February 2024

Categories |

RSS Feed

RSS Feed